1 July 2026

The UK Has Forgotten How to Build Innovative Things

The UK gave rise to the industrial revolution, Whittle’s Jet Engine, Colossus, the World Wide Web and the ability to fix a Land Rover Defender with duct tape. No nation has a deeper claim to having invented the modern world.

A classic Defender 110, reborn as an EV restomod — designed in Britain, increasingly rebuilt everywhere else. Image: Motor1

{kind=link}

Yet today the UK — still home to world-class universities, a deep(ly underpaid) engineering talent pool, and stated ambitions to be a science and technology superpower — has lost the capacity to actually build physical products. Hardware, manufactured goods, systems that exist in the real world: all in quiet, structural decline.

This is not a funding problem. It’s an incentive problem.

Where the Money Goes

Public R&D spending in the UK flows overwhelmingly toward established institutions: universities, large research organisations, and incumbent defence and technology firms. These entities are good at producing research outputs — papers, patents, conference presentations. They are not necessarily good at producing products.

This distinction matters. A research output advances knowledge. A product solves a problem for someone willing to pay for it. The UK has an abundance of the former and a growing deficit of the latter, particularly in hardware.

The grant ecosystem reinforces this. Innovate UK, UKRI, and their constituent bodies evaluate applications on academic rigour, novelty, and institutional credibility. What they don’t evaluate well is product viability, deployment readiness, or whether anyone actually needs the thing being built. The result is a pipeline that selects for organisations skilled at writing grant applications rather than organisations skilled at building products.

Over time, this creates a secondary distortion: small, agile companies learn to optimise for grant acquisition rather than product-market fit. They structure their roadmaps around funding cycles rather than customer needs. They hire grant writers instead of production engineers. The incentive structure turns potential product companies into quasi-academic research units, extending development timelines and consuming resources without producing deployable capability.

The Manufacturing Gap

The UK’s manufacturing base has contracted for decades. Manufacturing has fallen from roughly 30% of GDP in 1970 to around 8% today1 — 8.5% of total economic output as of Q1 20262 — and the employment picture is starker still: from over a third of the workforce in the post-war era to under 9% now.3 This is well documented and widely lamented, but the implications for innovation are underappreciated.

When you can’t manufacture domestically, you can’t iterate quickly. Prototyping requires overseas suppliers with minimum order quantities, shipping delays, and communication friction. The feedback loop between design and production — the loop that drives rapid improvement — stretches from days to months. And for hardware startups, where capital is scarce and runway is short, those months are fatal.

China understood this decades ago. Its innovation advantage in consumer electronics is not primarily about cheap labour — it’s about proximity. Designers sit next to manufacturers. A revision can be turned around overnight. The cost of experimentation is so low that companies can afford to try ten approaches and ship the one that works. To be clear about where this bites: prototyping from the UK is now genuinely fast — a Shenzhen fab will turn assembled boards around in under two weeks. The gap opens at the next stage. Going from ten units to ten thousand means design-for-manufacture iteration, tooling revisions, yield debugging — work that happens best standing on the factory floor, and that a UK founder does over email, time zones, and flights. That’s where proximity compounds, and where the UK has nothing to offer.

Rebuilding domestic manufacturing capacity is a long-term project that sits well outside the scope of innovation policy alone. But innovation policy could at least stop making the problem worse. Supporting small-batch domestic manufacturing, investing in shared prototyping facilities, and reducing the cost of (and actually funding) early-stage hardware iteration would all help close the gap between having an idea and having a product.

Who Gets Left Out

The structural bias toward institutions has a human cost. The people best positioned to build applied hardware products — experienced engineers, technical founders, people who’ve spent years working with real systems, even cough recent graduates cough — are often the worst positioned to access institutional support.

They don’t have academic affiliations. They don’t have matched funding. They don’t have prior grant history. They may not have degrees from the right universities, or degrees at all. What they have is the ability to design, build, and ship a product that works. And here the objection writes itself: the mechanisms exist, don’t they? Smart Grants never required a university affiliation. SEIS and EIS exist. Start Up Loans exist. But existing on paper is not the same as being accessible in practice. Start Up Loans cap out at £25k of personal debt — a rounding error against hardware tooling costs. SEIS presupposes you can find investors, and the UK’s early-stage investors are overwhelmingly software-literate and hardware-illiterate: they don’t know how to diligence a mixed-signal board, so they pattern-match on the one signal they can read — the university crest on the founder’s LinkedIn. The mechanisms that nominally serve unaffiliated founders funnel, in practice, back to the same golden-triangle pipeline.

This is not a meritocracy problem in the abstract. It’s a structural exclusion problem with concrete consequences. Every year, capable engineers look at the funding landscape, conclude there’s no viable path for them, and either take a salaried job at a large company, leave the country or go into finance. The ideas they would have built stay in notebooks. The products that would have existed don’t. The sovereign capability that would have resulted never materialises.

We Fund Pedigree and Existing Businesses

The numbers make the concentration explicit. Of the UK’s venture-backed university spinouts, Cambridge accounts for 144, Oxford for 129, and Imperial for 664 — the golden triangle dominates spinout value creation, and roughly 80% of VC firms sit in London.5 The entire commercialisation apparatus — tech transfer offices, proof-of-concept funds, university venture arms — is built around the assumption that innovation begins inside an elite institution and is spun out of it. If you’re an engineer with industry experience and a working prototype, but no academic affiliation to OxBridge/Imperial, that apparatus likely ignores you if they even see you at all.

The grant system compounds this. Most Innovate UK grants require match funding of 25–55% of project costs,6 which presupposes existing capital or investors — precisely what an unaffiliated founder lacks. Worse, funding is paid quarterly in arrears, meaning applicants need enough working capital to fund the project upfront and wait for reimbursement.6 This is a system designed for organisations with balance sheets, not individuals with capability. Even Innovate UK has tacitly conceded the point: Smart Grants were paused from January 2025,7 with the replacement scheme reportedly intended to address criticisms of administrative burden, low success rates, and misalignment with business needs.8

Meanwhile, the policy conversation remains fixated on the institutional pipeline. The 2023 independent spinout review focused on university equity terms — negotiations on university stakes were starting at an average of 34%9 — and this year’s follow-up review calls for UKRI to boost proof-of-concept funding to £100 million annually.10 Both are reasonable. Both also channel yet more support through universities, to founders already inside the system.

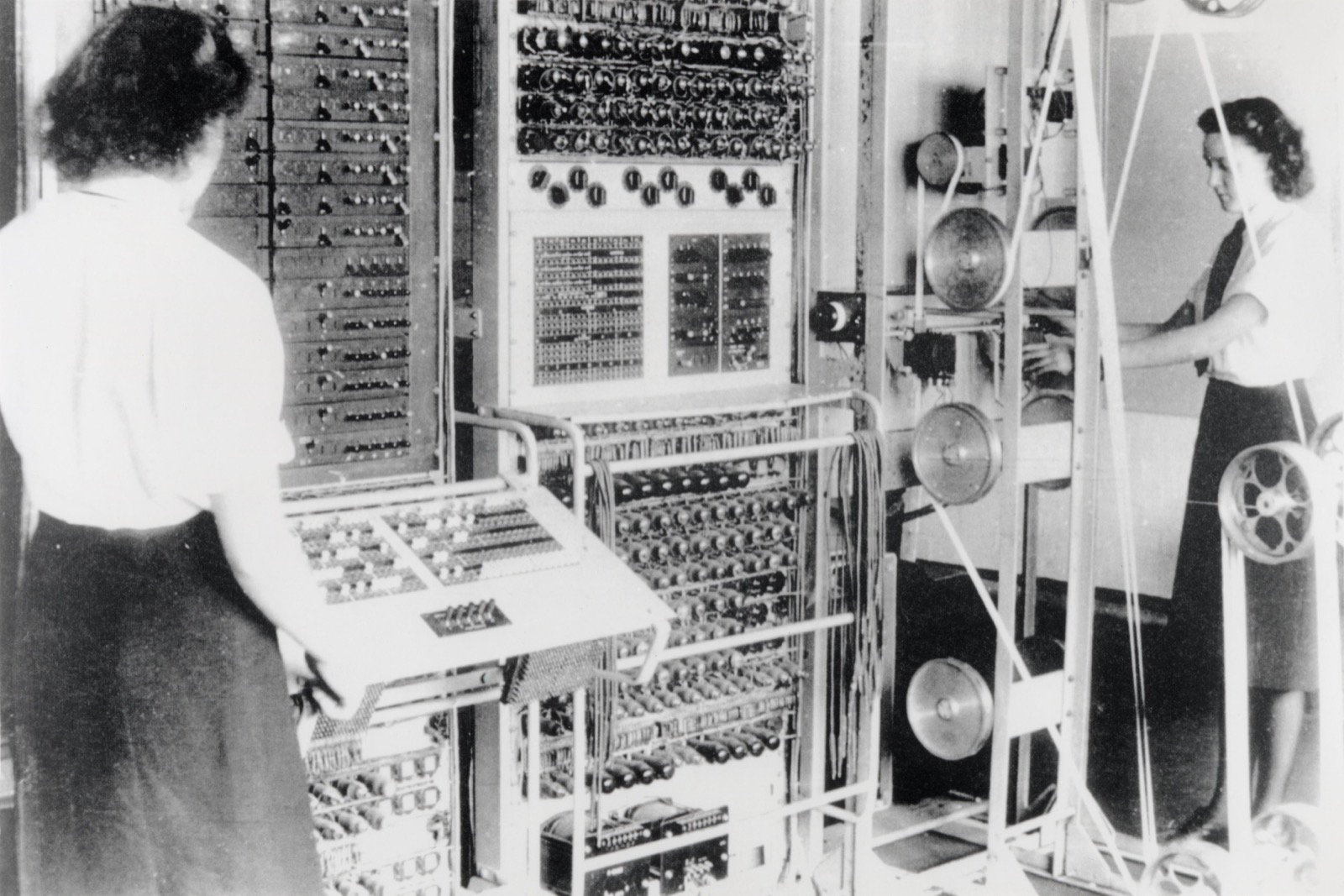

Colossus Mark 2 at Bletchley Park, 1943 — the world’s first programmable electronic computer, built in eleven months. Image: Wikimedia Commons, public domain

{kind=link}

It wasn’t always like this. In 1941, Alan Turing and three Bletchley Park colleagues wrote directly to Churchill to say the codebreaking effort was being strangled by lack of staff and resources. Churchill’s response, the same day: “Make sure they have all they want on extreme priority” … give them what they want.

No match funding. No quarterly reimbursement in arrears. No institutional letters of support. The state saw demonstrated capability and moved in hours. Eighty-five years later, the same state would ask Turing for a 30% match contribution and pay him back quarterly, in arrears, subject to audit.

What would the fix look like? Funding that starts where an engineer with nothing but skill can start — design files, simulations, prior work — and scales through milestones to hardware, judged by practitioners rather than letterheads. To be discussed in further depth in follow up pieces.

What Building Actually Requires

Building things — physical things, at scale, that work reliably in the real world — requires a specific set of conditions. It requires access to components and manufacturing. It requires short feedback loops between design and testing. It requires funding that’s small, fast, and non-bureaucratic at the earliest stages.

It requires a system that evaluates people on what they can demonstrate, not on which institution vouches for them. A graduate from the bottom of the league table who can design a four-layer mixed-signal board and get it manufactured is, for the purposes of sovereign hardware capability, worth exactly as much as an Imperial spinout founder with the same skills. The current system prices them very differently.

The UK has none of these conditions for hardware founders operating outside institutional frameworks. And until it does, the gap between the country’s research output and its manufacturing capability will continue to widen.

The government talks about strategic autonomy, sovereign capability, and reducing dependence on foreign supply chains. These are the right goals. But they are incompatible with an innovation infrastructure that funds papers over products, rewards credentials over capability, and makes it structurally impossible for a talented engineer with no institutional backing to build the things the country says it needs.

The UK hasn’t lost the ability to build things. It’s lost the ability to let people build things.

Footnotes

- World Bank, Manufacturing, value added (% of GDP) — United Kingdom; see also Pettinger, T., “Relative decline in UK manufacturing”, Economics Help (2025). data.worldbank.org/indicator/NV.IND.MANF.ZS?locations=GB ↩

- House of Commons Library, Manufacturing industries: Economic indicators (June 2026). commonslibrary.parliament.uk/research-briefings/sn05206 ↩

- ONS labour market data, summarised in Economy of the United Kingdom: manufacturing employment fell from ~36.5% of the labour force (1841–1961) to 8.9% by the 2010s. ↩

- Royal Academy of Engineering spinout analysis, reported in Research Professional News, “UK spinout success broadening beyond golden triangle” (June 2026). researchprofessionalnews.com ↩

- BVCA, The State of UK Venture Capital (2024). burges-salmon.com/articles/102jrrz/the-state-of-uk-venture-capital ↩

- Innovate UK funding rules and grant guidance, UKRI: R&D grants typically fund up to 70% of eligible costs for SMEs (i.e. 30%+ match), paid quarterly in arrears. ukri.org/councils/innovate-uk/guidance-for-applicants/general-guidance/funding-rules ↩

- UKRI, Smart Grants funding guidance: programme paused from January 2025. ukri.org/councils/innovate-uk/guidance-for-applicants/guidance-for-specific-funds/smart-innovation-funding-guidance ↩

- Hodgson, D., “Innovate UK’s Funding Slowdown in 2025”, RedKnight Consultancy (June 2025). redknightconsultancy.co.uk ↩

- Tracey, I. & Williamson, A., Independent Review of University Spin-out Companies, HM Treasury/DSIT (November 2023). gov.uk/government/publications/independent-review-of-university-spin-out-companies ↩

- Hickson, T., Deepening University-Investor Links, UKRI (February 2026), reported in Times Higher Education. timeshighereducation.com ↩